March 2026 was difficult for markets. West Asia tensions, soaring oil, and falling indices tested every investor’s resolve. Here is what the data says — and how a rules-based model can quiet the noise in your head.

“The investor’s chief problem — and even his worst enemy — is likely to be himself.” — Benjamin Graham, The Intelligent Investor

01 — WHAT HAPPENED

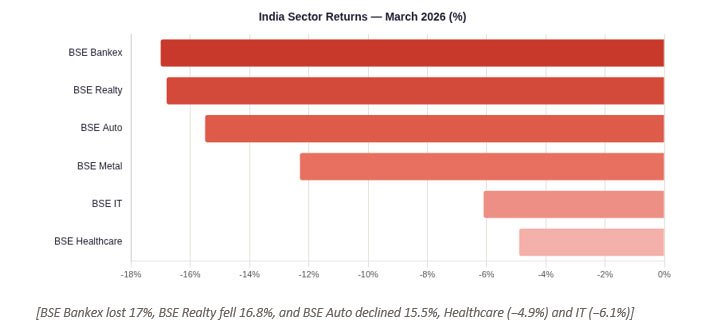

March 2026: A Month the Markets Would Rather Forget

Escalating West Asia tensions disrupted shipping through the Strait of Hormuz, a chokepoint for over 20% of global oil supply, pushing crude oil prices above $100 per barrel for the first time in recent memory. The resulting spike in energy prices, coupled with currency pressure and foreign fund outflows, triggered a cascading reaction across markets worldwide. What started as a geopolitical event quickly became an economic reality that markets had to price in, fast.

No market was spared. If you checked your portfolio during March and felt a knot in your stomach, that reaction is deeply human. The instinct to “do something”, sell, exit, pause SIPs, is one of the most natural responses to financial uncertainty. And yet, it is often a costly one.

02 — THE BEHAVIOURAL PROBLEM

Why Our Brains Are Wired to Make Bad Investment Decisions

Behavioural finance research consistently shows that investors tend to sell near market bottoms and buy near market peaks — the exact opposite of what creates wealth. This isn’t a failure of intelligence. It’s a feature of how human beings process risk and uncertainty.

When headlines scream “war,” “oil crisis,” and “market crash,” the instinct to exit, pause SIPs, or move everything to fixed deposits feels rational. Historically, it is one of the most costly decisions an investor can make.

“The stock market is a device for transferring money from the impatient to the patient.” — Warren Buffett

The antidote is not willpower. It is a framework that makes the decision before emotions arrive.

03 — THE FRAMEWORK

Introducing the Equity Valuation Index (EVI)

The EVI, developed by ICICI Prudential AMC, answers a simple but powerful question: at this moment, are Indian equities cheap, fairly valued, or expensive? It blends four equally-weighted parameters:

● P/E Ratio – How much investors are paying per rupee of corporate earnings

● P/B Ratio – Market price relative to the book (accounting) value of assets

● G-Sec × P/E – Equity premium over government bond yields — the opportunity cost of being in equities

● Market Cap/GDP – How large the stock market is relative to the economy — the “Buffett Indicator” of overall valuation

04 — READING THE SIGNAL TODAY

EVI POSITION — FEBRUARY VS MARCH 2026

In February 2026, the EVI stood at ~108.8 — in the Neutral band. After the March sell-off, it moved to ~97, shifting into the “Invest in Equities” zone. The market’s pain had, objectively, created value. This is not a guarantee of near-term returns. What the EVI offers is something rarer: a data-backed anchor when the emotional pull to act defensively is at its strongest.

This is the kind of signal that gets drowned out by the noise of daily news — but historically, it has been among the most important ones to pay attention to.

To put this in context: over the 20-year history of the EVI (2006–2026), periods where the index dipped into the “Invest in Equities” zone have consistently been associated with above-average forward returns over a 3–5 year horizon, based on back-tested data. The EVI hit its deepest levels during the 2008–09 subprime crisis, the 2016 European crisis, and the March 2020 COVID sell-off — all of which, in hindsight, were generational buying opportunities.

05 — BEHAVIOURAL GUIDANCE

How the EVI Keeps You From Being Your Own Worst Enemy

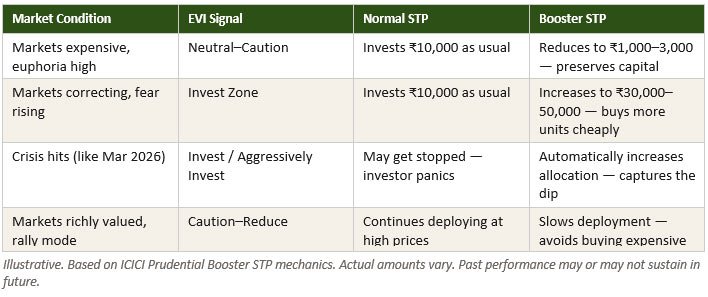

The real power of a model like the EVI is not just informational, it is behavioural. When markets fall sharply and fear dominates headlines, the EVI gives you a framework to answer the question every investor is silently asking: “Should I stop my SIPs / STPs? Should I move everything to Fixed Deposits? Or should I actually be doing the opposite?”

One concrete application of this principle is the Booster STP, a facility that links your monthly equity investment amount directly to the EVI reading:

The system does the behavioural heavy lifting for you. It is the difference between a compass and a mood — the compass doesn’t panic; the mood does.

06 — THE BIGGER PICTURE

India’s Structural Story Remains Intact

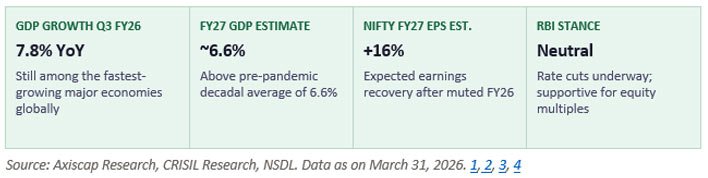

Geopolitical events, by their nature, create acute stress that feels permanent but rarely is, from a long-term economic standpoint. India’s fundamentals, as of March 2026, continue to reflect structural strength:

08 — THE PRACTICAL PATH FORWARD

What This Means for Your Investment Journey

No model predicts how long geopolitical uncertainties persist. What 20+ years of market data says, with consistency, is the following:

1. Don’t pause SIPs in a falling market: Every paused SIP during a downturn is a missed opportunity to buy units at lower prices. The math of rupee cost averaging works best precisely when it is most uncomfortable.

2. Let valuation signals, not headlines, guide deployment: If you have idle savings in a liquid or debt fund, the current EVI reading in the “Invest in Equities” zone historically suggests this may be a reasonable time to consider staggered deployment into equities.

3. Volatility ≠ Permanent Loss: Volatility is the price of admission for long-term equity returns. The Nifty 50 has recovered from every major crisis — 2001, 2008, 2020 — to reach new highs. March 2026 is a chapter, not the ending.

4. Asset allocation is your seatbelt: If you have the right mix of equity, debt, and gold suited to your risk profile, a 10–15% equity correction should feel bumpy — not catastrophic. The correction is the system working, not failing.

The Best Investors Are Boring Ones

History’s most consistent wealth creators, whether individual investors or fund managers, share a trait that is deeply unglamorous: they do not treat market crises as emergencies. They treat them as scheduled events in a long journey, because that is precisely what the data tells us they are.

If you have questions about your specific portfolio, your asset allocation, or how to think about deploying idle funds in this environment, we encourage you to speak with your advisor. These conversations are most valuable when markets are unsettled, not after they’ve recovered.

Stay invested. Stay allocated. Stay the course.