What the COVID cycle revealed about disciplined investing

In Part 1 of this series, we explored how an Investment Policy Statement (IPS) helps bring structure, clarity, and discipline to long-term investing. We also looked at how allocation bands and Min-Max studies help portfolios stay aligned to intended levels of risk over time.

But the real value of any investment framework is rarely visible during calm markets.

It becomes visible during stress.

During rising markets:

● concentration feels rewarding,

● diversification feels unnecessary,

● and risk feels manageable.

During falling markets:

● panic feels rational,

● long-term thinking weakens,

● and investors often make permanent decisions based on temporary conditions.

And few periods tested investor behaviour more sharply than the COVID market cycle of 2020.

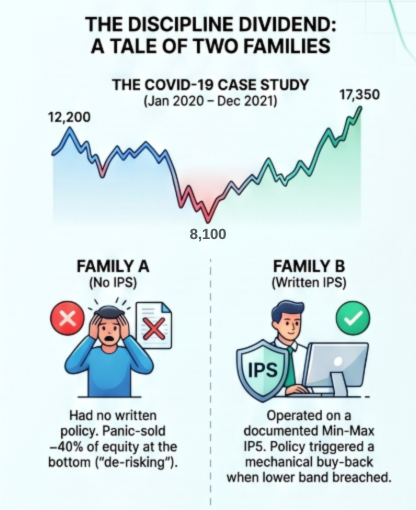

Between January and March 2020, the Nifty 50 fell from nearly 12,200 to the levels of ~8,100 in just a few weeks. Headlines turned deeply pessimistic, uncertainty was extreme, and even experienced investors found themselves questioning long-term strategies. Yet by the end of 2021 (Nifty 50 – 17,350), Indian markets had staged one of the strongest recoveries in recent history.

What became evident during this period was not simply the unpredictability of markets, but the enormous difference investor behaviour can make to long-term outcomes.

Two Investors. Same Markets. Very Different Outcomes.

Let’s take an example of a useful comparison between two investors navigating the same COVID cycle.

Both investors began with similar portfolio structures and long-term objectives. But their experience through the market correction looked very different.

Investor A: Operating Without a Defined Framework

Before the correction, equity exposure had gradually drifted upward after a strong market rally. There were no clearly defined allocation bands or rebalancing triggers. As markets fell sharply in March 2020, anxiety increased quickly.

Without a written framework anchoring decisions, the natural response became defensive:

● reduce risk,

● move to cash,

● and “wait for clarity.”

Large portions of equity exposure were reduced near the lows.

The problem, however, was not the intention. It was timing.

By the time confidence returned, markets had already recovered significantly. Re-entering became emotionally difficult because prices no longer “felt attractive.”

The result was a portfolio that participated fully in the decline — but only partially in the recovery.

Investor B: Operating With a Structured Framework

The second investor also experienced the same market decline. But the portfolio operated within predefined allocation bands.

As equity exposure fell below the lower allocation threshold during the correction, the framework triggered a review and phased rebalancing process.

Importantly, this was not based on predicting a market recovery. It was based on maintaining alignment to the portfolio’s intended structure. Rather than attempting to “time” the market, the portfolio gradually moved back toward its strategic allocation.

As markets recovered through 2020 and 2021, the portfolio remained invested and participated more fully in the rebound.

The difference between the two investors was not intelligence, access, or product selection.

It was the presence of a framework before volatility arrived.

These ideas may sound simple. But during volatile markets, they become remarkably difficult to practise consistently without structure.

What Risks IPS Frameworks Are Actually Designed to Prevent

An IPS is often misunderstood as a technical investment document. In reality, many of its most important benefits are behavioural and practical.

A well-designed framework helps reduce the likelihood of:

● excessive concentration in one asset class or strategy,

● unintended portfolio drift,

● emotionally driven allocation changes,

● liquidity mismatches,

● and reactive decision-making during market extremes.

For example, a portfolio that performs exceptionally well in equities over several years may gradually become far more aggressive than originally intended. Without periodic reviews or allocation bands, this change can go unnoticed until volatility returns.

Similarly, investors sometimes discover only during periods of stress that they were carrying excessive exposure to one sector, one style of investing, or even one fund house.

The purpose of an IPS is not to eliminate risk.

It is to ensure risks remain intentional, visible, and aligned to the investor’s broader financial goals.

Why Rebalancing Often Feels Uncomfortable — But Matters

Good portfolio management can occasionally feel counterintuitive.

During strong markets, rebalancing may require trimming assets that have performed very well. During declines, it may involve gradually increasing exposure when sentiment feels negative.

Emotionally, this rarely feels natural. But over long periods, this discipline prevents portfolios from drifting too far from their intended structure.

Institutional investors rely heavily on this—not because they predict markets better, but because they recognize that consistency often matters more than reacting emotionally to short-term movements.

What You Can Do Now

If you’re reflecting on your own portfolio after reading this:

● Check for portfolio drift

Compare your intended allocation to today’s reality.

● Identify hidden concentrations

How much sits with one fund house? One investment style? One sector? Concentration builds quietly during good years.

● Know your rebalancing trigger

Does your portfolio have a written rule for when to rebalance, or does it happen when someone “feels” it’s time?

● Understand risk capacity, not just tolerance

Tolerance is how you feel about volatility. Capacity is how much you can afford to lose without derailing your plan.

Structure doesn’t guarantee returns. But it creates the conditions for disciplined decision-making when markets test your resolve.

In Part 3, we’ll explore how investors can make an IPS practical, how portfolios are reviewed over time, how to think about risk capacity, and how disciplined investing evolves across different life stages.