Why structure, discipline and allocation bands matter more than most people realise

Most investors believe successful investing comes from picking the right funds at the right time. The research tells a different story.

Why This Conversation Matters

93.6%

Asset allocation explained 93.6% of the variation in portfolio returns in the landmark BHB study of U.S. pension funds, highlighting the importance of portfolio structure over individual investment selection.

Behaviour Matters

Research from DALBAR has consistently shown that investors often earn less than the investments they own because decisions made during periods of fear and optimism can interrupt long-term compounding.

≈3%

Vanguard’s Advisor’s Alpha research suggests that disciplined practices such as portfolio construction, rebalancing, and behavioural coaching may add approximately 3% of annual value over time.

This is where an Investment Policy Statement (IPS) becomes valuable.

An IPS is not a product recommendation document or a one-time risk questionnaire. It is a written framework that defines:

● what the portfolio is trying to achieve,

● how much risk makes sense,

● how investments should broadly be allocated,

● and how decisions should be made when markets become uncertain.

In simple terms, it helps connect investments to real-life priorities — retirement, children’s education, liquidity, wealth preservation, or financial independence — before emotions and market noise begin influencing decisions.

A well-designed IPS usually includes:

● investment objectives and timelines,

● acceptable risk levels,

● strategic asset allocation,

● allocation ranges or “bands,”

● liquidity needs,

● concentration limits,

● and review or rebalancing guidelines.

But perhaps its most valuable role is behavioural.

Markets will always fluctuate. An IPS helps ensure the portfolio does not fluctuate emotionally along with them.

Why Allocation Matters More Than Most Investors Think

One of the biggest misconceptions in investing is that portfolios remain balanced automatically.

They do not.

A portfolio that begins with:

● 60% equity,

● 30% debt,

● and 10% gold

can quietly become:

● 75% equity,

● 18% debt,

● and 7% gold

after a prolonged equity rally.

Nothing appears visibly wrong. In fact, the investor often feels more confident because returns have been strong. But the portfolio may now be carrying materially higher risk than originally intended.

This gradual shift is called portfolio drift.

And it is one of the primary reasons institutional investors across the world rely heavily on allocation frameworks and portfolio bands.

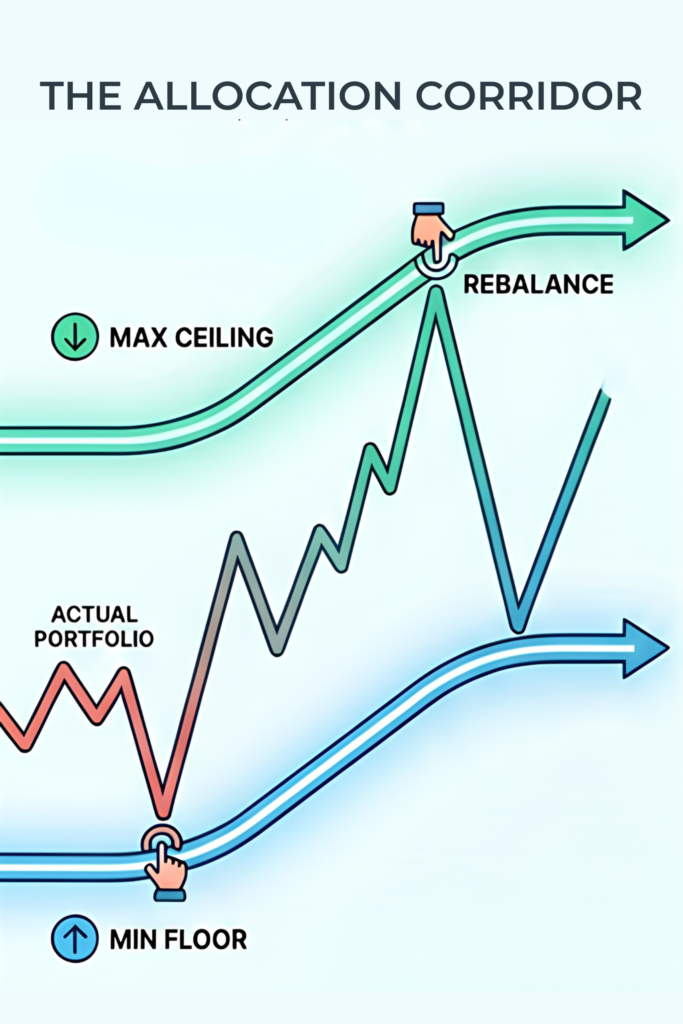

The Min-Max Study: Keeping Portfolios Aligned

An essential part of many IPS frameworks is something called a Min-Max study. Rather than treating allocation as a fixed number, portfolios operate within predefined ranges.

For example:

● Equity: 60–75%

● Debt: 20–35%

● Gold: 5–10%

These ranges are called allocation bands.

The purpose of these bands is simple: they help investors stay aligned to their intended level of risk while still allowing portfolios to naturally move with markets. Each range shows the portfolio’s intended allocation,

current position, and whether it remains aligned to the investor’s long-term risk framework.

If equity rises materially beyond the upper band, the portfolio may require trimming or rebalancing. If markets correct sharply and equity falls below the lower band, the framework may suggest gradually increasing exposure again.

This approach removes a large part of emotional decision-making from investing.

Instead of asking: “What do we feel like doing in this market?”

the framework asks: “What does the portfolio structure require us to do?”

That difference becomes extremely important during volatile periods.

Why Bands Instead of Exact Numbers

Institutional portfolios rarely operate with rigid instructions such as: “Equity must always remain exactly 70%.” Markets move daily. Fixed numbers create false precision.

Bands recognize two realities: markets are dynamic, and investor behaviour is emotional.

Bands create flexibility without losing discipline. They let portfolios participate in market movements while maintaining guardrails around risk. Importantly, bands aren’t about predicting markets. They’re about ensuring portfolios don’t unintentionally drift into levels of risk you never planned to take.

The Behavioural Advantage of a Structured Portfolio

The strongest investment frameworks are often behavioural frameworks in disguise. Because the biggest risk to long-term wealth creation is not always volatility itself, but how investors respond to volatility. An IPS helps create distance between emotion and action. It does not eliminate uncertainty. But it can create structure during uncertain periods, which is often where the greatest value of disciplined investing emerges.

As you think about your own investing journey, consider:

How much of your portfolio reflects deliberate decisions versus the natural accumulation of investments over time?

Have your financial priorities changed more than your portfolio has?

If markets became significantly more volatile tomorrow, would your investment decisions be guided more by conviction or emotion?

Because the value of structure is often invisible when markets are rising. It tends to become most visible when uncertainty arrives.

In Part 2, we’ll explore how two investors experienced the COVID market cycle very differently despite starting with similar portfolios, and how written frameworks help prevent the most common risks investors unknowingly take over time.