Why disciplined investing is less about prediction and more about adaptation

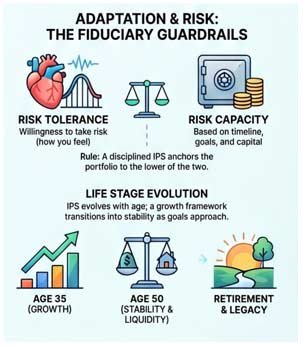

A portfolio created at 35 should not look identical at 50.

The goals change. Responsibilities change. Liquidity needs change. Risk changes.

And perhaps most importantly, an investor’s priorities, perspective, and relationship with risk evolve. Many portfolios continue operating on assumptions from a very different phase of life. As priorities evolve from growth to stability, liquidity, or specific goals, portfolios need periodic reassessment, not just because markets change, but because life does too.

That is one of the most important roles an Investment Policy Statement (IPS) can play over time.

Good Portfolio Reviews Are About More Than Performance

Most investors review portfolios through one lens: “How much return did we generate?”

While important, that is only one part of the picture. Meaningful portfolio reviews should also ask:

● Has my life changed?

● Has my portfolio become materially riskier?

● Are my liquidity needs different today?

● Has concentration quietly increased?

● Are my upcoming goals now closer than before?

● Does my portfolio still reflect my priorities?

These questions matter because a portfolio that was perfectly suitable five years ago may no longer be appropriate today, even if returns were excellent.

This is especially relevant today, as investors increasingly balance multiple financial priorities while also planning for longer financial lifespans than previous generations. That changes how risk, liquidity, and long-term planning need to be approached.

The Difference Between Risk Tolerance and Risk Capacity

One of the most misunderstood aspects of investing is risk. Most investors define risk emotionally: “I am comfortable with equity.” But real portfolio construction goes deeper than emotional comfort alone.

There is a difference between:

● the risk an investor is emotionally willing to take,

● and the risk they are financially capable of taking.

An IPS helps create clarity around this by aligning goals, timelines, liquidity, and risk exposure within a broader long-term framework.

Why Rebalancing Often Feels Counterintuitive

One of the challenges of disciplined investing is that good decisions often feel uncomfortable in the moment. During strong rallies, rebalancing may require trimming assets that continue performing well. During corrections, it may involve gradually increasing exposure when uncertainty feels highest.

This is why many investors struggle with consistency. According to AMFI industry data, SIP stoppage ratios often rise during volatile periods as investors react emotionally to short-term uncertainty.

But over long periods, rebalancing is less about predicting markets and more about ensuring portfolios remain aligned to their original goals and risk framework.

Why Some of the Biggest Portfolio Risks Build Quietly

Most investors assume risk arrives dramatically. In reality, many portfolio risks build slowly:

● excessive concentration in one asset class,

● dependency on one investment style,

● illiquidity,

● unmanaged exposure to one sector,

● or portfolios carrying more equity risk than originally intended.

The challenge is that these risks often feel comfortable while markets are rising. This is why structured frameworks matter. An IPS helps create predefined guardrails around:

● allocation ranges,

● liquidity needs,

● concentration exposure,

● and review discipline.

Not because uncertainty can be eliminated. But because portfolios benefit from structure when emotions become unreliable.

A Good IPS Evolves Along With the Investor

An IPS shouldn’t remain frozen in time.

As life evolves, portfolios should evolve thoughtfully alongside it. For some, that means gradually increasing stability as retirement approaches. For others, creating liquidity for business opportunities or family responsibilities.

The framework remains valuable because it creates continuity through those transitions—not by predicting the future, but by ensuring decisions continue reflecting the investor’s actual life, not just current market sentiment.

Making It Practical:

Whether you have a formal investment framework or not, these are questions worth revisiting from time to time:

● Has my portfolio evolved in line with my life?

Major life events, changing goals, or increasing responsibilities often warrant a fresh look at your investments.

● Do I understand the level of risk I’m taking today?

A portfolio can become materially different from what you originally intended simply because markets have performed well.

● Is my portfolio sufficiently diversified?

Concentration often builds gradually, whether by asset class, sector, geography, or individual investments.

● When was the last time I reviewed my portfolio beyond returns?

A meaningful review considers goals, liquidity needs, risk, and time horizons—not just performance.

● Do I have a clear basis for making investment decisions during periods of market uncertainty?

Whether written down or not, having a consistent framework is often more valuable than reacting to headlines.

Final Thought

An Investment Policy Statement isn’t about adding complexity. It’s about creating clarity.

Clarity around what you’re investing for. Clarity around how much risk makes sense. Clarity around what triggers action versus what’s just market noise. Because it helps ensure the portfolio you’re building today is still the portfolio you need five, ten, or twenty years from now. And that consistency, over time, is often what separates wealth that compounds from wealth that drifts.