Preheader: Understanding the Difference Between Investment Advice and Distribution in India Financial Planner. Wealth Manager. Investment Advisor. Wealth Advisor. Portfolio Consultant.

You’ve likely come across these titles across websites, business cards, and platforms like LinkedIn. While they describe the nature of services offered, it’s important to understand that these titles themselves are not formally defined or regulated by SEBI.

What is defined are the underlying regulatory registrations that determine how a financial professional operates, how they are compensated, and what obligations they have toward you.

For most retail investors, two commonly encountered categories are:

● SEBI Registered Investment Adviser (RIA)

● Mutual Fund Distributor (MFD)

Understanding the distinction between these two can help you make more informed financial decisions.

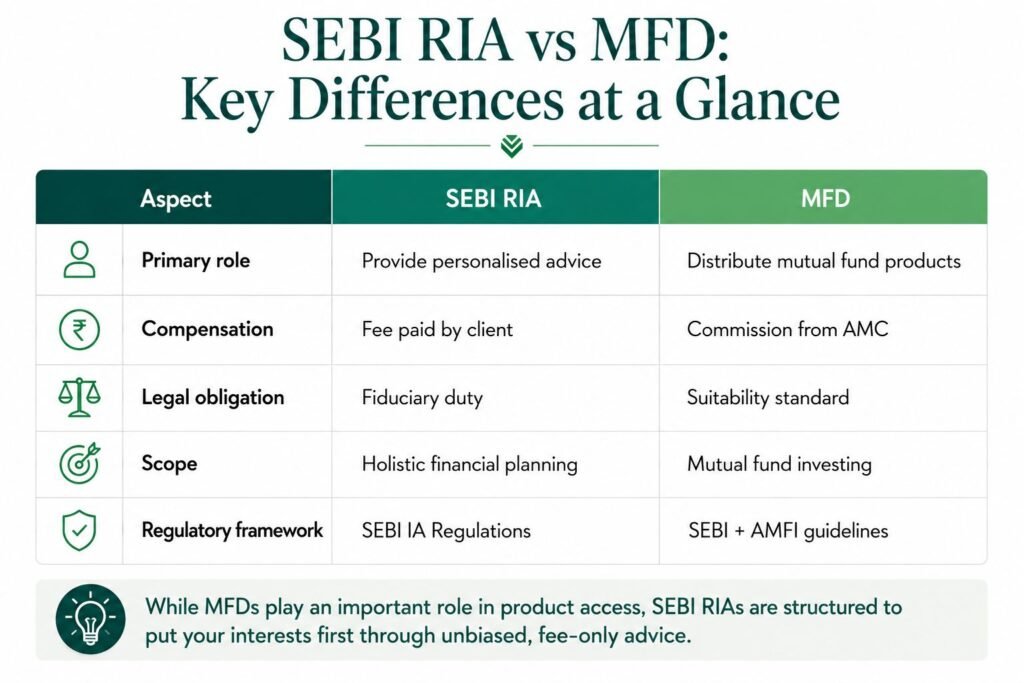

The SEBI Registered Investment Adviser (RIA)

Advice-driven, fee-based engagement

A SEBI Registered Investment Adviser (RIA) is authorised under the SEBI (Investment Advisers) Regulations, 2013 to provide personalised investment advice for a fee. RIAs operate under a fiduciary obligation, which means they are required to act in the best interest of their clients.

Key characteristics:

● Provide holistic financial advice (investments, goals, risk profiling, asset allocation, etc.)

● Earn fixed fees directly from clients

● Cannot receive commissions or incentives from product manufacturers for advisory clients

● Must adhere to strict disclosure, suitability, and compliance standards

The Mutual Fund Distributor (MFD)

Execution and product distribution focused

A Mutual Fund Distributor (MFD) is registered with AMFI (Association of Mutual Funds in India) and operates within a regulatory framework overseen by SEBI. MFDs facilitate investments into mutual fund schemes and play an important role in expanding retail participation in capital markets.

Key characteristics:

● Help investors select and transact in mutual fund schemes

● Earn trail commissions from Asset Management Companies (AMCs)

● Compensation is embedded in the expense ratio of Regular plans

● Operate under a suitability standard when recommending products

Many investors benefit from the accessibility, handholding, and continuity that MFDs provide, especially when starting their investment journey.

Advice vs Distribution — The Core Difference

The distinction between RIAs and MFDs is not about better or worse; it is about different engagement models.

Both models serve important purposes. The right choice depends on your expectations, preferences, and the type of relationship you want with your financial professional.

About Titles Like “Financial Planner” or “Wealth Manager”

These are service descriptions, not regulatory categories. An RIA may use these titles to describe the scope of services offered. MFDs, on the other hand, are expected to avoid using titles that could imply advisory services, unless appropriately registered. As an investor, it is useful to look beyond titles and understand the underlying registration and model.

Three Questions Worth Asking

Before engaging any financial professional, consider asking:

● Are you registered with SEBI as an investment adviser or with AMFI as a distributor?

● What is the nature of your obligation toward me (advisory or distribution)?

● How are you compensated: via fees or commissions?

These questions bring clarity to how the relationship works.

Why This Distinction Matters

Different compensation models can lead to different approaches:

● A fee-based model focuses on ongoing advice and planning

● A commission-based model focuses on facilitating access to investment products

Neither is inherently right or wrong, but understanding the structure helps you choose what aligns with your needs.

A Balanced Perspective

India’s financial ecosystem has grown significantly due to the contributions of both RIAs and MFDs. MFDs have played a critical role in increasing mutual fund penetration, while RIAs bring a structured, advice-led approach for investors seeking comprehensive financial planning. The right choice ultimately depends on the complexity of your finances, your preference for guidance versus execution, and whether you’re comfortable paying for advice explicitly or indirectly, because in investing, how you choose matters just as much as what you choose.

So, are you investing based on what’s convenient or what’s truly aligned with your financial future?